Why 2027 Is a Pivotal Year for SA Buy-to-Let Investors

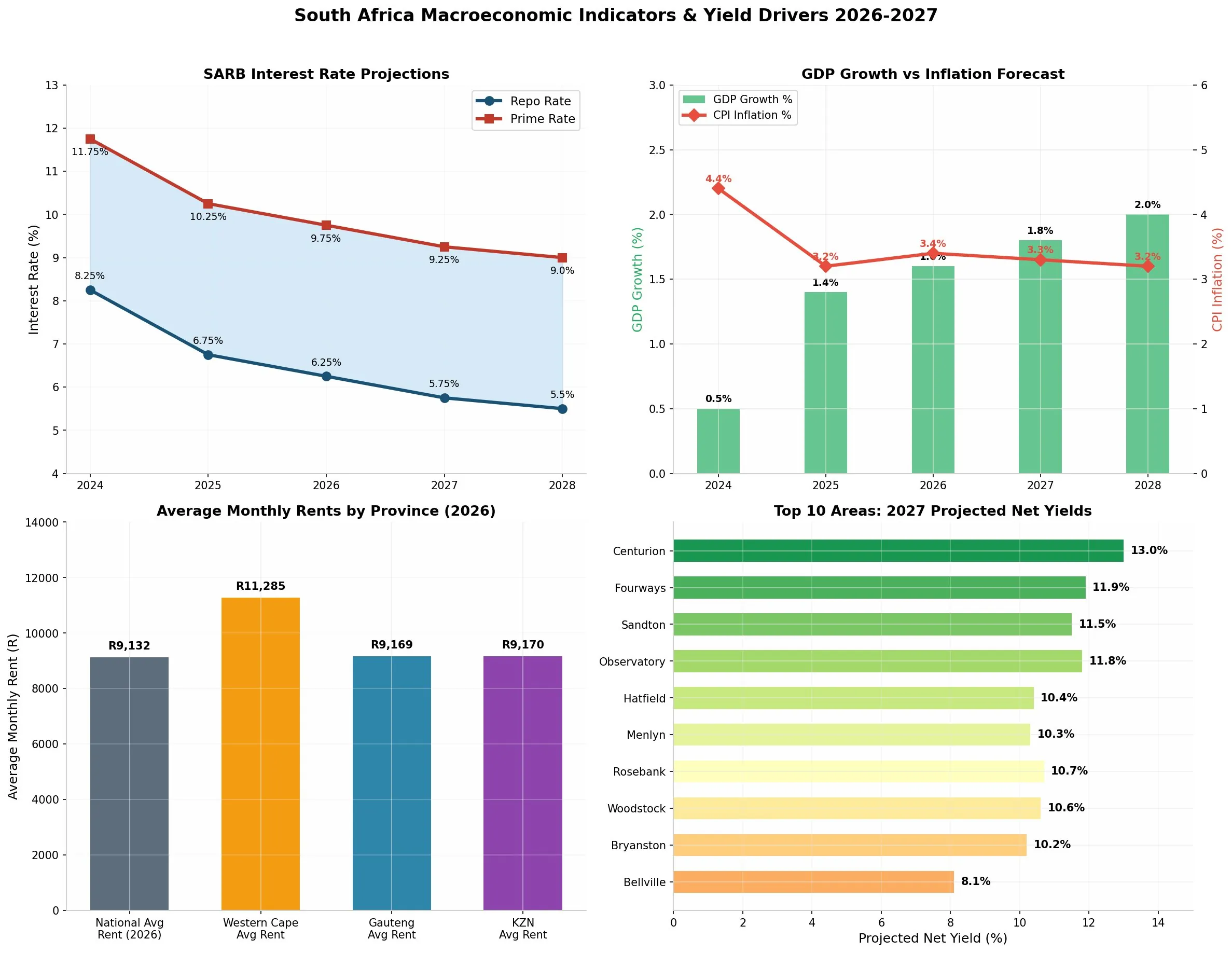

South Africa's property market is entering a structural inflection point. After years of aggressive interest rate hikes that peaked at a repo rate of 8.25% in 2024, the SARB embarked on an easing cycle — cutting rates six consecutive times. However, on 28 May 2026 the MPC reversed course, hiking the repo rate by 25bp to 7.00% with prime now at 10.50%, citing intensifying inflation risks. Analysts continue to project a return to cuts once inflation stabilises, with some forecasting the repo ending 2027 at 5.75% — but the timing is now less certain.

This monetary policy pivot, combined with GDP growth accelerating from 0.5% in 2024 to a projected 1.8% in 2027, creates a rare convergence of conditions favouring buy-to-let investors:

- Cheaper debt servicing — higher cash-on-cash returns on leveraged properties

- Stabilising inflation at 3.3% (within SARB's target band) — predictable rental escalations

- Improving tenant affordability — lower arrears and vacancy risk as household budgets ease

- Infrastructure investment in energy, water and transport — property value support across key nodes

For investors asking "Where should I buy rental property in South Africa in 2027?" — this article delivers a data-driven, city-by-city projection using rental yield data, macroeconomic forecasts, vacancy rates, tenant demand drivers, tax implications and infrastructure pipelines.

Methodology: How We Built These Projections

Our projections integrate five data layers:

1. Current Rental Yield Data (2026 Baseline)

Net yields calculated from PayProp, Lightstone and ooba data after deducting: 8% vacancy allowance, 9% management fee, municipal rates and taxes, maintenance (1–2% of property value annually), and insurance and levies.

2. Macroeconomic Forecasts

- SARB repo rate: 7.00% (May 2026, following 25bp hike) — further path uncertain; analyst consensus ~5.75% by end-2027 if inflation stabilises

- GDP growth: 1.6% (2026) → 1.8% (2027) → 2.0% (2028)

- CPI inflation: 3.4% (2026) → 3.3% (2027)

- National unemployment: 31.9% (improving slowly)

3. Rental Market Dynamics

- National average rent: R9,132/month (2026)

- Western Cape average: R11,285/month (highest nationally)

- Gauteng average: R9,169/month | KZN average: R9,170/month

- Tenant arrears: 17.2% in Q3 2025 — elevated but stabilising

4. Supply and Demand Indicators

- Cape Town vacancy rate: 1.07% (2024) — lowest on record

- Johannesburg vacancy: 7–8% average — higher but stable

- Foreign buyer activity: Over R1 billion in Cape Town premium areas (Jan–May 2025)

5. Tax and Regulatory Environment

- Personal income tax threshold: R99,000 (2026/27)

- CGT annual exclusion: R50,000

- Primary residence CGT exclusion: R3 million

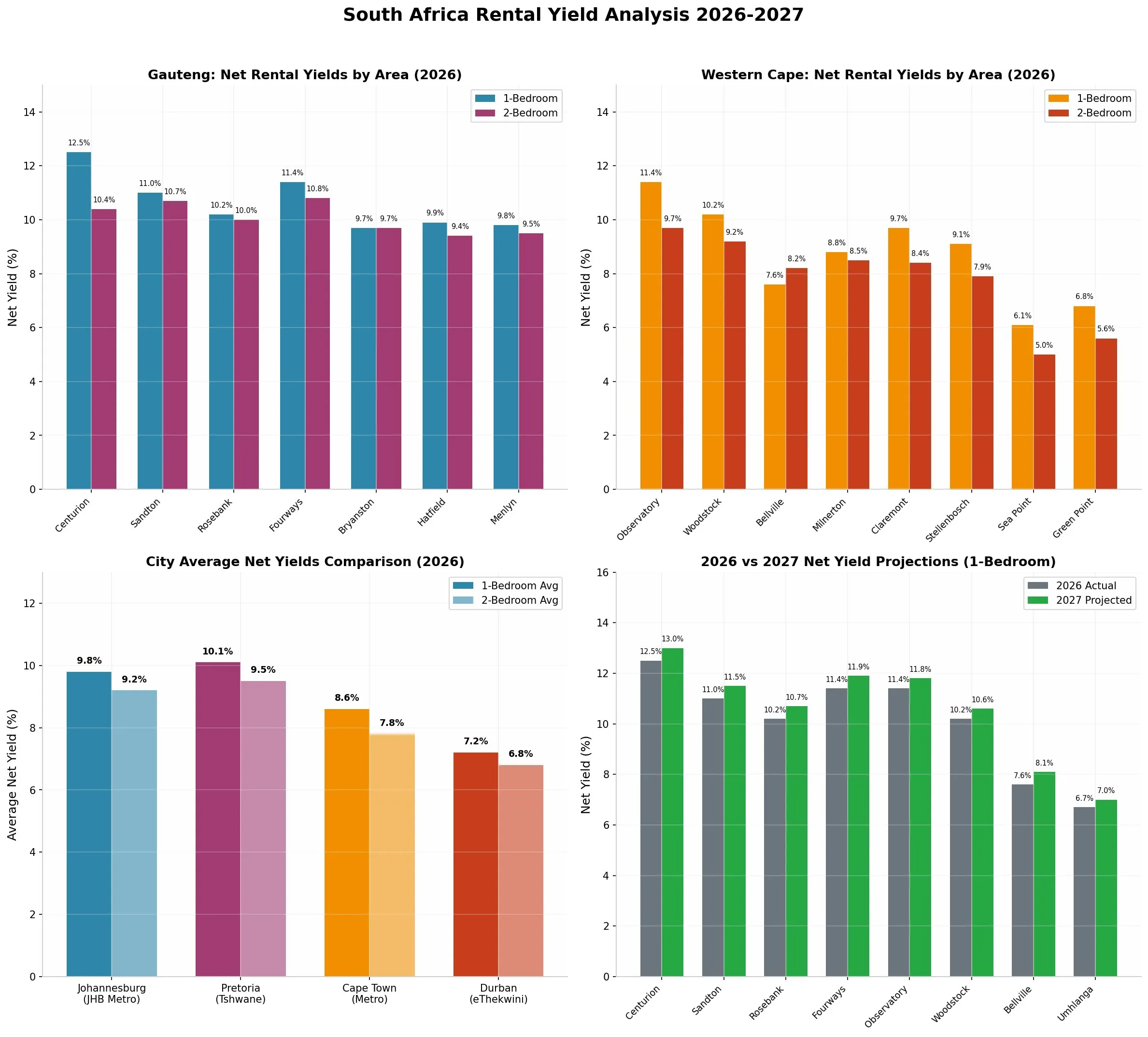

Top 10 Rental Yield Areas for 2027 — Quick Summary

🏆 2027 Net Yield Rankings (1-Bedroom Apartments)

| Rank | City / Area | 2026 Net Yield | 2027 Projected | Entry Price |

|---|---|---|---|---|

| 🥇 | Centurion (Pretoria) | 12.5% | 13.0% | R620,000 |

| 🥈 | Fourways (Johannesburg) | 11.4% | 11.9% | R750,000 |

| 🥉 | Sandton (Johannesburg) | 11.0% | 11.5% | R900,000 |

| 4 | Observatory (Cape Town) | 11.4% | 11.8% | R920,000 |

| 5 | Rosebank (Johannesburg) | 10.2% | 10.7% | R1,150,000 |

| 6 | Woodstock (Cape Town) | 10.2% | 10.6% | R1,050,000 |

| 7 | Hatfield (Pretoria) | 9.9% | 10.4% | R650,000 |

| 8 | Menlyn (Pretoria) | 9.8% | 10.3% | R850,000 |

| 9 | Bryanston (Johannesburg) | 9.7% | 10.2% | R1,750,000 (2-bed) |

| 10 | Bellville (Cape Town) | 7.6% | 8.1% | R820,000 |

Key Data Visualisations

Figure 1: SA Rental Yield Analysis 2026–2027 — net yields by area for Gauteng and Western Cape, city average comparison, and 2027 projected yields

Figure 2: Macroeconomic Indicators and Yield Drivers — SARB rate trajectory, GDP vs inflation, average rents by province, and top 10 2027 net yield projections

See where your number lands. Enter your property's price and rent to get its exact net yield and compare it to the city rankings above.

Rental Yield Calculator →City-by-City 2027 Rental Yield Projections

🥇 1. Pretoria (Tshwane) — The Yield Capital of South Africa

2026 City Avg: 10.1% | 2027 Projected: 10.6%Pretoria emerges as South Africa's undisputed yield champion in 2027, driven by two powerhouse nodes and the lowest entry prices among major yield areas.

Centurion — The Standout

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R620,000 | R645,000 |

| 1-Bed Monthly Rent | R7,600 | R8,100 |

| Gross Yield | 14.7% | 15.1% |

| Net Yield | 12.5% | 13.0% |

Why Centurion dominates: Lowest entry price among major yield areas, with Menlyn Maine and Centurion Mall driving sustained tenant demand. Proximity to Gautrain, N1/N14 highways, and the Waterfall City spillover effect. Strong tenant base of young professionals and students from the University of Pretoria and Tshwane University of Technology. Lower body corporate levies than Sandton or Rosebank.

Hatfield — Student Rental Powerhouse

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R650,000 | R675,000 |

| 1-Bed Monthly Rent | R6,800 | R7,300 |

| Net Yield | 9.9% | 10.4% |

Hatfield benefits from virtually guaranteed demand from the University of Pretoria and embassies in the diplomatic quarter. Vacancy is structurally low. The Gautrain station adds a second tenant demographic of CBD commuters who prefer to avoid Pretoria CBD crime risks.

Menlyn — New Development Hub

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R850,000 | R885,000 |

| 1-Bed Monthly Rent | R8,700 | R9,300 |

| Net Yield | 9.8% | 10.3% |

🥈 2. Johannesburg — Yield Meets Liquidity

2026 City Avg: 9.8% | 2027 Projected: 10.3%Johannesburg offers the best combination of high yield and investment liquidity in South Africa. The city's depth of tenant demand — from corporate relocations, young professionals, and the service sector — means well-located properties rarely sit vacant.

Fourways — The High-Yield Surprise

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R750,000 | R780,000 |

| 1-Bed Monthly Rent | R8,500 | R9,100 |

| Net Yield | 11.4% | 11.9% |

Fourways punches well above its weight for yield. The Fourways Mall precinct, Montecasino, and corporate campuses generate consistent professional tenant demand while prices remain accessible relative to Sandton.

Sandton — Blue-Chip Yield

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R900,000 | R940,000 |

| 1-Bed Monthly Rent | R10,300 | R11,000 |

| Net Yield | 11.0% | 11.5% |

Rosebank — Premium Yield

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R1,150,000 | R1,200,000 |

| 1-Bed Monthly Rent | R12,200 | R13,000 |

| Net Yield | 10.2% | 10.7% |

Bryanston — Best 2-Bedroom Value

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 2-Bed Purchase Price | R1,750,000 | R1,820,000 |

| 2-Bed Monthly Rent | R17,800 | R19,000 |

| Net Yield | 9.7% | 10.2% |

Johannesburg 2027 Outlook: Rate cuts stimulate demand from first-time tenants upgrading from shared accommodation. Corporate office market recovery drives Sandton and Rosebank. Midrand and Waterfall City infrastructure investment adds a new high-yield corridor to monitor.

Modelling at current rates? Calculate your exact monthly repayment at prime 10.50% — and see how the projected 2027 rate path changes your cash flow.

Bond Repayment Calculator →🏅 3. Cape Town — Stability, Growth and Selective Yield

2026 City Avg: 8.6% | 2027 Projected: 9.0%Cape Town defies the conventional wisdom that lower yields mean worse investments. With the lowest vacancy rate in the country (1.07%), strong foreign buyer demand, and consistent semigration from Gauteng and KZN, Cape Town offers something Johannesburg and Pretoria cannot: price resilience and capital growth certainty.

Observatory — Cape Town's Yield Leader

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R920,000 | R960,000 |

| 1-Bed Monthly Rent | R10,900 | R11,700 |

| Net Yield | 11.4% | 11.8% |

Observatory offers Cape Town's strongest yield due to proximity to UCT, Groote Schuur Hospital, the CBD, and the emerging creative and tech sector. Building and complex selection is critical — established complexes outperform individual units significantly.

Woodstock — Creative Economy Hub

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R1,050,000 | R1,095,000 |

| 1-Bed Monthly Rent | R11,000 | R11,700 |

| Net Yield | 10.2% | 10.6% |

Woodstock's gentrification trajectory and creative-sector tenant base support strong rents. Security and building quality due diligence is essential — the gap between well-managed and poorly-managed stock is wider here than in most suburbs.

Sea Point and Green Point — Lifestyle, Not Yield

| Area | 2026 Net Yield | 2027 Projection | Strategy |

|---|---|---|---|

| Sea Point (1-Bed) | 6.1% | 6.4% | Capital preservation |

| Green Point (1-Bed) | 6.8% | 7.1% | Capital preservation |

These areas are capital preservation plays — foreign buyers committed over R1 billion here in early 2025. Yields are modest but capital growth and liquidity are the highest in the country.

4. Durban (eThekwini) — The Recovery Story

2026 City Avg: 7.2% | 2027 Projected: 7.6%Durban offers attractive gross yields (8–10% in northern suburbs) but higher operating costs and vacancy risk compress net returns below those of Johannesburg and Pretoria. The recovery from the 2021 July unrest and ongoing municipal service delivery challenges continue to weigh on investor confidence, though improving sentiment is visible.

Durban North and Glenwood

| Metric | 2026 | 2027 Projection |

|---|---|---|

| Gross Yield Range | 8–10% | 8.5–10.5% |

| Net Yield (Est.) | 5.5–7% | 6–7.6% |

Umhlanga — Premium Coastal

| Metric | 2026 | 2027 Projection |

|---|---|---|

| 1-Bed Purchase Price | R1,230,000 | R1,280,000 |

| 1-Bed Monthly Rent | R9,000 | R9,400 |

| Net Yield | 6.7% | 7.0% |

Umhlanga is stable but yield-compressed — better suited to investors prioritising lifestyle, capital growth and tenant stability over maximum cash flow.

The 2027 Yield Equation: 5 Forces Driving Projections

1. Interest Rate Trajectory — The Strongest Driver

The SARB's easing cycle is the single biggest tailwind for 2027 yields. Every 25bps rate cut reduces bond servicing costs by approximately R150–R300 per month on typical buy-to-let properties, improves cash-on-cash returns by 0.3–0.5 percentage points, and expands the buyer pool — supporting property values without compressing rents.

Projection: Repo rate falling from 7.00% to 5.75% by end-2027 adds approximately 0.5–0.8 percentage points to net yields on leveraged properties across all markets.

2. Inflation and Rental Escalations

With CPI projected at 3.3% in 2027 — well within SARB's 3–6% target band — rental escalations of 5–7% are achievable without tenant affordability strain. This outpaces inflation, improving real returns year-on-year.

3. Infrastructure and Development

- Waterfall City — R100bn project, 28,000 units by 2027, creating a new high-demand node

- Gautrain expansion to Soweto and Pretoria west — new transport corridors drive rental demand

- Renewable energy rollout reducing load shedding frequency and severity

- Road upgrades (N1, N3, N2) improving commuter access to key rental nodes

4. Tenant Affordability

Disposable income after rent and debt payments fell to 20.9% in 2025. As interest rates decline and real wages recover, tenant affordability improves — meaning lower arrears, shorter vacancy periods, and more stable yields for landlords across all tiers.

5. Tax Efficiency

The 2026 Budget introduced several pro-investor changes: higher personal income tax threshold (R99,000), increased CGT exclusions (R50,000 annual, R3m primary residence). Small portfolios generating rental income below R99,000 net may pay zero tax — making buy-to-let highly tax-efficient at the entry level.

Property Type Strategy: What to Buy in 2027

| Property Type | Avg Net Yield | Tenant Depth | Maintenance Risk | Liquidity |

|---|---|---|---|---|

| 1-Bed Apartment | 10.5% | Medium | Low | High |

| 2-Bed Apartment | 9.8% | High | Low | High |

| 3-Bed House | 7.5% | Medium | High | Medium |

| Studio | 11.0% | Low | Low | Medium |

Our recommendation: 2-bedroom sectional-title units in secure, well-managed complexes offer the best risk-adjusted yield. They attract a broader tenant pool — couples, sharers, small families, and remote workers — with manageable levies and lower maintenance risk than freehold houses.

What to avoid in 2027:

- 3-bedroom freehold houses in premium suburbs (Parkhurst, Houghton, Sea Point) — yields drop to 3.6–5.5% net

- Oversupplied CBD buildings with poor sectional title management or high special levy risk

- Student-only properties without professional tenant management backup

Tax Considerations for 2027 Buy-to-Let Investors

For South African Residents

Rental income is taxable, but deductible expenses reduce the effective tax burden significantly. Deductible items include:

- Bond interest (full amount deductible against rental income)

- Municipal rates and body corporate levies

- Insurance and maintenance costs

- Agent management fees (typically 8–10%)

- Depreciation on fixtures and fittings

The personal income tax threshold of R99,000 (under 65) means small portfolios may effectively pay zero tax after deductions — making entry-level buy-to-let highly efficient.

For Foreign Investors

- Taxed only on South African-sourced income

- Non-resident CGT withholding: 7.5% for individuals, 10% for companies

- Must register with SARS as a non-resident taxpayer before receiving rental income

- Primary residence CGT exclusion (R3m) may apply in limited circumstances — professional advice is essential

Risk Factors That Could Derail 2027 Projections

| Risk | Probability | Yield Impact |

|---|---|---|

| SARB pauses rate cuts due to oil or FX shocks | Medium | −0.5 to −1.0% |

| Municipal service collapse (water/electricity) | Medium-High (regional) | −1.0 to −2.0% |

| Recession (GDP below 1%) | Low | −0.8 to −1.5% |

| Oversupply in specific nodes (Waterfall, Midrand) | Medium | −0.3 to −0.8% |

| Tenant arrears spike above 20% nationally | Medium | −0.5 to −1.0% |

| New property taxes or levies introduced | Low | −0.2 to −0.5% |

Conclusion: Your 2027 Buy-to-Let Action Plan

South Africa's rental market in 2027 presents a rare alignment of monetary easing, economic recovery, and yield opportunity. Here is the strategic roadmap based on the data:

- Target Pretoria (Centurion, Hatfield, Menlyn) for maximum yield — 10.4–13.0% net

- Target Johannesburg (Fourways, Sandton, Rosebank, Bryanston) for yield combined with liquidity — 10.2–11.9% net

- Target Cape Town (Observatory, Woodstock) for yield and capital growth balance — 10.6–11.8% net

- Buy 2-bedroom sectional-title units in well-managed, secure complexes for optimal risk-adjusted returns

- Calculate net yield — not gross yield — using your actual bond repayment, rates, levies and vacancy assumptions before any purchase

- Monitor the macro indicators — repo rate, CPI and GDP growth will move the market; quarterly recalibration is worth the effort

The data does not lie: Centurion at 13% net, Fourways at 11.9%, Observatory at 11.8% — these are compelling numbers in any investment context. Use them as starting points for your own due diligence, not as guarantees.

🚀 Calculate Your Specific Property's Numbers

Every property is different. Use our free calculators to run the numbers on any property with your actual purchase price, bond repayment, rates, levies and vacancy assumptions.

💡 Ready to Finance Your Next Investment Property?

Bond originators compare multiple banks simultaneously — and it costs you nothing. SA's most established originators:

Affiliate disclosure: we may receive a referral fee if you apply through these links, at no cost to you.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Rental yields are projections based on current data and macroeconomic forecasts. Actual returns may vary. Always conduct independent due diligence and consult a qualified financial advisor before making investment decisions.